Commercial real estate owners and operators all over the world are using proptech as the latest weapon in the real estate industry’s fight to be more sustainable. “PropTech,” is the term used to describe the broad application of technology to real estate markets. It refers to the myriad tech companies working to transform the real estate industry, based on a rapidly changing digital landscape and ever-shifting consumption trends and patterns.

PropTech aims to make owning, leasing, or working in a building easier and more efficient for everyone, whether it be through reducing paperwork for property management or streamlining transactions between tenants and landlords.

In this article, we will focus specifically on how property technology offers a unique opportunity to enhance operations while simultaneously reducing carbon and energy footprints at new and existing buildings.

Energy-Efficient Properties

Energy-efficient properties or smart buildings are the structure that uses technology to automate a building’s operations including lighting, heating, and security. Smart buildings increase efficiency to minimize energy waste.

PropTech conserves energy by automatically adjusting the lighting, temperature, and ventilation based on the requirements at a particular time. The research suggests the energy expenditure accounts for almost 19% of the total operational cost of a building. For most of the small-scale and medium-size companies, a 10% reduction in energy can positively impact their profitability by 1.5%.

Reducing Waste

Understanding and optimizing energy output of buildings is only one of the ways that properties can reduce their carbon emissions and achieve more sustainable operations. There is also a growing need to measure, understand, and eliminate the waste that ends up in our landfills and oceans. Waste management solutions present a great opportunity for properties to reduce their waste at a larger scale and make a substantial impact.

Why Develop Proptech?

Technological innovation has revolutionized several other industries and now we can’t imagine living without Uber, Venmo, Doordash and so much more. The same benefits — streamlined efficiency, better customer experience, simpler processes and of course sustainability — can and should be apparent in the real estate industry. With PropTech, companies are trying to address these pain points and introduce an innovative edge at every step and revitalize existing systems.

To learn more about LeasePilot and get the latest on commercial real estate trends

Lawyers and legal professionals are trained to be highly skeptik and are often hesitant to adopt technology. And in today’s post pandemic reality, legal teams are being forced to make the technology transition quicker than ever.

Implementing a product while changing team habits and culture can be challenging, but after helping many successfully adopt LeasePilot’s technology, we have gathered a few key tactics that help companies quickly utilize new technology.

Set Expectations & Goals with Your Service Provider

With any new technology it takes time before you can start maximizing your return on investment. Most companies will have a plan to expedite your user experience but it is important to make your expectations are aligned beforehand.

Ensure you communicate what your main goals are for the platform to your new service provider, that way the onboarding team can tailor the implementation process accordingly. It helps when everyone is on the same page about why you purchased the product in the first place.

Internal Communication

It’s important to prepare your team when adopting a new piece of technology, especially those who will see a significant shift in their day-to-day tasks.

Involving the team in the implementation process is often a good way to make them feel included in the new decision, and it empowers them to steer the project in a direction that ensures they are receiving the value they need from the project.

Be sure to clearly communicate the reasons you purchased the technology with the team, such as the problems you’re looking to overcome or the goals you would like to achieve.

Understanding the Implementation Process

An implementation strategy should be in place to help you understand the benefits the technology has to offer. We encourage you to work closely with the product’s Customer Success team as they have been through the process of new adoption many times and are aware of the common blockers for new users. If a part of their strategy doesn’t make sense to you, or if you typically learn in a particular way, communicate that to them so they can adjust their strategies accordingly.

Allow your Team Time to Adjust

While it is important to be considerate that adopting new technology often comes with an adjustment period, try to maintain structure throughout the process.

Don’t hesitate to put deadlines on accomplishing certain milestones. Customer Success teams can usually help you determine what is realistic and achievable.

We find it can be useful for everyone to block time towards implementing technology on their own after training sessions. This allows users to become independent and move at a steady pace with the technology. When you go too long between training and putting the training into practice, it significantly decreases the efficiency of the learning process.

Check In

We encourage you to ask your team to provide feedback and share that feedback with the provider. It is also important to attend each of the scheduled sessions as a part of the implementation process so that you don’t lose momentum.

These check-ins are critical for early successes, trust us when we say that no support team is setting meetings just for the sake of hitting a quota. These are usually well-planned and impactful.

Stay Up to Date

It is important to stay in the loop when it comes to your technology provider for updates and important improvements. When updates happen, take a few minutes to browse and see if any new feature could work for you. After all, these updates are built around the user.

If you have questions about how a feature can benefit you or your firm specifically, the Customer Success team should be able to point you in the right direction!

Like incorporating any new habit into your routine, adopting new technology for your team can be tough. It takes courage to try something new, resilience to keep going, and optimism to see the big picture. But the payout can be huge for those who can incorporate a new tool or process, usually seen with improvements in efficiency, communication, and collaboration.

To learn more about LeasePilot and get the latest on commercial real estate trends

According to a survey conducted by LegalBillReview.com, almost every in-house legal team is desperate to reduce the amount spent on outside counsel. Managing outside counsel spend enhances your law department’s credibility within the company, making you more valuable and less likely for budget slashing.

Seeking cost-saving solutions may seem like an easy task, but it can actually be quite challenging. For a more viable way to reduce outside counsel spend, take a look at our approach below.

Evaluate Resources

It is important to ensure that only the right work is reaching the desks of outside counsel. This will mean something different to every company, but the factors to consider are specialization, complexity, risk, and scope.

Automate What you Can

Legal departments often spend too much time completing tasks that don’t necessarily require a law degree to complete. These requests are typically low-risk, low-complexity, and often repetitive that have no business taking up unnecessary time.

There are hundreds of systems out there that are designed to complete these timely tasks for you quickly and error free. Typically, all it takes is a bit of organizing, standardization and implementation.

Set a Budget

Budgets help you benchmark and control spending with ballpark figures. Once you are operating within a budget, you start to question how much certain vendors cost and whether or not they are earning their keep. Start by looking at expenses from previous years to set ballpark figures/estimates. Next, you should talk to people from other departments to spot issues that may affect spending. And lastly, ask your vendors what the costs for upcoming matters will look like.

Track Performance Through KPIs

Measuring KPIs enables businesses to understand the performance and health of their team so that critical adjustments can be made to achieve strategic goals. Knowing and measuring the right KPIs will help achieve results faster and more effectively. Legal teams create huge amounts of value for an organization, but that story is often lost through ineffective communication. Lawyers think in paragraphs, executives think in metrics. If lawyers can’t convert their ideas and activities into a framework their colleagues can understand, then their story goes untold.

Using software to manage legal spend is one of the best lines of defense against rising legal costs. For more legal software solutions, consider an automation tool like LeasePilot to improve efficiencies with lease drafting and time management.

To learn more about LeasePilot and get the latest on commercial real estate trends

There is a perception that smartphones, social media apps and technology in general can cause distractions at work, however, technology in the workplace isn’t all that bad after all. If used properly and productively, technology can drastically improve the rate in which you and your business achieve your goals. Here are some ways modern devices and applications increase efficiency and productivity in the workplace.

Technology Automates Workflow

Many successful businesses utilize powerful tools and applications that enable them to streamline complex workflows and processes. These technologies are often built with productivity in mind and have the capability to facilitate repetitive and time-consuming tasks such as collecting and sorting information or paying bills.

Various industries and business functions utilize numerous business automation tools that are designed to make things run more efficiently and effectively. For example, Yardi is a property management software and services to optimize every aspect of their operations. Their software comes in different packages and allows real estate operators to manage accounting, operations and more with ease. Meanwhile, LeasePilot, the first and only software platform engineered exclusively for commercial leasing allows lawyers, paralegals, and leasing admins to generate an error-free lease first draft in about 30 minutes.

Turning over recurring and antiquated tasks to powerful computers increases productivity as well as reduces the chance for human error. What’s more, letting technology do the heavy lifting allows you and your employees to focus on core business tasks and revenue-generating activities.

Technology Allows for Seamless Communication

As remote work continues to be the new normal, cloud and mobile technologies remain essential for companies with distributed workforces to stay connected and productive no matter where they are.

The most used method of communication among remote teams is text. Text messages can be easily indexed and searched in an instant. One of the most popular text-based collaborative tools is Slack. It replaces email, text messaging, and instant chat messages under a single unified offering. Slack is available in Web-based and mobile app versions, enabling teams to collaborate the way they want.

Another method is audio-video collaboration tools. Although face-to-face videoconferencing has some inherent disadvantages, this practice offers many benefits, as well. Videoconferencing is a great way to bridge the communication gap in a remote-work setting. Microsoft’s Skype is one of the most popular video conferencing tools. It offers powerful features for sharing messages, codes, and files among individuals and groups. Zoom is another powerful contender in this category.

Enables Strategic Time Management

Proper time management is one way to ensure that you and your employees get the most out of your workday. Calendar and scheduling applications such as Google Calendar integrate with almost every kind of productivity app and are instantly accessible on any device. Simply plot your tasks and do your best to complete these within their designated timelines. Setting reminders can help keep you on track and develop good habits.

To learn more about LeasePilot and get the latest on commercial real estate trends

Like every other industry, the commercial real estate business experienced significant change at the onset of the pandemic. From the rapid adoption of technology and streamlining internal processes, the industry doesn’t show signs of slowing down. So, what are the next real estate technology market trends? The following are just a few of the many examples of trends that are shaping the property industry.

Technology Stays on Top

Property technology (proptech) is advancing faster than ever before. Between 2015 and 2019, proptech has grown by 1072%, and in 2018, $8.3 billion was invested in the digital field. This amount is projected to grow.

According to the same report, 56% of the industry said that the pandemic revealed vulnerabilities and shortcomings in their company’s digital capabilities and technology in the real estate industry.

COVID-19 offered a tremendous case study in how real estate companies with agile, scalable, and redundant processes in place are able to weather the storm with confidence. Whether it’s your sales team, finance team, or operations team, there are lots of fantastic software solutions out there that are purpose-built to help modernize the core processes of a given business unit.

LeasePilot, for example, is the first and only software platform engineered exclusively for commercial leasing. LeasePilot’s automation tools give lawyers, paralegals, and leasing admins the power to generate an error-free first draft in about 30 minutes.

Data Security

Although the property industry remains traditional in nature, we are still seeing a massive transition toward new technologies. Because of this, we have seen the creation of large amounts of data, which is only expected to increase. This creates the new challenge of keeping all of this data secure.

From personal tenant information to sensitive property and transactional data – protection is needed all around. Government regulations on data collection and use are one way of addressing these challenges but they are not enough. Many startups are emerging that are offering software solutions to monitor cyberattacks on buildings, encrypt data collected by IoT devices, and more.

Property Management Software

Many startups are developing cloud-based customer relationship management (CRM) platforms for real estate firms and agents. These CRM platforms help agents keep track of their clients and ongoing deals as well as keep related documentation secure. Being cloud-based, these platforms are easily accessible, making important data available when needed.

For example, HqO is transforming the commercial real estate space through its tenant experience platform and mobile application. The HqO tenant experience platform centralizes tenant experience initiatives and building technologies on one application. It offers features like event scheduling for office employees, ordering takeout through the platform, giving them transportation updates, secure visitor management, and more.

The trends outlined above are just a few of the major breakthroughs we will see more of in 2022. The commercial real estate world is operating at an unprecedented speed and LeasePilot among many other innovative companies that are making a difference. Implementing emerging technologies into your business goes a long way in gaining a competitive advantage. To learn more about LeasePilot and its products visit here.

To learn more about LeasePilot and get the latest on commercial real estate trends

When we think of technology, empathy is not something that often comes to mind. But as we’ve all come to learn, COVID-19 changes everything. The pandemic has drastically increased the rate in which people are adopting technology and now, empathy in tech is more important than ever. Lawyers and legal professionals who have historically hesitated to adopt technology in the past are now being forced to make the transition quicker than ever in today’s new reality.

With the use of automated tools and processes, there is a perception that people are being replaced by technology. But, the legal profession was built on people, and empathy is a vital component for the profession of law to function. If legal technology is going to be successful, people, and most certainly empathy, must be involved.

Empathy Builds Trust

Empathy builds trust; it creates an experience that is based on more than just a transaction. Empathy is the foundation needed for anything to work – including legal tech solutions.

Integrating empathy means absorbing a true understanding of the user’s needs and building technology around them. The result should be meaningful, meet market demands, and allow legal professionals to perform their work with ease.

How LeasePilot’s Technology was Built on Empathy

Tech companies don’t have to lack authenticity.

LeasePilot’s commercial real estate roots run deep – The company was founded by former CRE attorneys. The Customer Success team, led by a former real estate general counsel, is staffed exclusively by real estate attorneys and senior paralegals. In short, LeasePilot knows the challenges you face, and is prepared to face them with you.

“Legal tech cannot be successful without true empathy for its users. Period. Legal professionals are trained to be highly skeptical and may therefore be more reluctant to adopt legal tech than most others, despite the value the tech may bring. The ability to authentically and intelligently overcome that reluctance will result from a development and delivery process that truly understands their needs and visibly demonstrates the value that legal tech can bring to their daily professional lives.”

Nadine Ezzie

Unlike other real estate tools, LeasePilot’s technology was designed with lawyers in mind. “Most technology is created by engineers and people that have an understanding of some big benefit or the generic concept of efficiency. But the tools that are being created actually make the end-user’s life harder,” Gabriel Safar said.

Empathy in Action

Imagine getting a deal done in 10 days that used to take 90. Printing automated abstracts rather than spending countless hours summarizing deal terms. Never re-keying the same information into multiple systems. Generating transactional reports for lenders, investors, and buyers rather than have lawyers read and re-read the underlying leases ad nauseum.

Because LeasePilot streamlines the entire process, both attorneys and non-attorneys can focus on what they do best and everyone wins.

Ultimately, the impact is radically more efficient markets that free up a massive amount of wasted human potential so it can be re-directed toward pursuing more meaningful objectives.

That is the role that empathy plays in technology.

To learn more about LeasePilot and get the latest on commercial real estate trends

The Best Commercial Real Estate Podcasts Worth Your Time

Kelly Barrett

Marketing Associate | LeasePilot

In today’s ever-changing market, staying up-to-date with the commercial real estate industry can be quite the challenge. While traditional media does a great job of covering the CRE industry, many of us can agree that podcasts are the best way to consume news while on the go.

To save time and remain in-the-know, you’ll find an excess of commercial real estate podcasts that cover everything from updates on the latest technology to market trends in CRE investing — and everything in between. Whether you listen during your commute, while working out, or in- between meetings, podcasts are an easy way to gain valuable insight into the world of commercial real estate.

Here are our top picks for the best commercial real estate podcasts:

America’s Commercial Real Estate Show

Michael Bull, Founder of Bull Realty, hosts this weekly podcast that has been broadcasting for nearly a decade. The podcast focuses on motivating real estate brokers, investors, leasing agents, and other professionals to increase their income and gain new insights into the world of CRE sales and investments. Michael picks guests ranging from economists, analysts and industry leaders who join him to share market intelligence, forecasts and strategies related to chosen weekly topics. The Commercial Real Estate Show consistently ranks as one of the best commercial real estate podcasts on the market.

The Real Estate Guys™ Radio Show

As one of the longest-running commercial real estate podcasts, The Real Estate Guys™ Radio Show definitely lands a spot on our list. Robert Helms, a professional investor, and Russell Gray, a financial strategist cover a wide-range of commercial real estate topics in a fun and engaging way. They combine their decades of expertise with wit and energy to produce a dynamic podcast that appeals to commercial real estate professionals worldwide. Their content often focuses on investment strategies and market trends, all of which are invaluable data to both brokers and agents.

Office Politics: The Battle For The Future Of Work with Bisnow

Bisnow’s five-part podcast series takes a deep dive into the new future of living with Covid. The show includes commentary from industry experts, business owners, and employees who examine questions on topics like equality, office relationships, climate change, and the evolution of cities.

New York Times The Daily

For most CRE professionals, finding time to catch up on news can be nearly impossible. This is where the New York Times Daily podcast comes in handy. Each Monday through Friday, this podcast drops 20-minute segments dedicated to breaking down the day’s most important news. This outlet is guaranteed to keep you up to date on what’s going on in the world and how it might affect the commercial real estate market.

The Propcast

The Propcast, by Louisa Dickins, Co-founder of LMRE the leading Global PropTech recruitment Consultancy and CREtech and REIMtech is another great addition to our list. The aim of this show is to introduce exciting global PropTech innovators and discuss how their work has created a shift in focus when it comes to digitising the built environment. If you are interested in finding out more about Proptech or are keen to know who the big players are that are moving and shaking the CRE industry, this is the podcast for you.

Retail Retold

The Retail Retold Podcast highlights community retailers’ stories across the country and gives a behind the scenes look at leaders in the commercial real estate industry. The podcast is led by Chris Ressa, an established industry influencer, recognized as one of Chain Store Age magazine’s 10 Under 40: Rising Stars of Retail Real Estate list, the show’s episodes contain valuable insights to help solve real estate needs for entrepreneurs and national retailers.

Want to Get the Latest on Commercial Real Estate Trends and Technology?

The legal industry has shifted significantly in recent years, and in-house legal teams are often at the heart of this shift. Among these changes come the need to get businesses to recognize the value in-house legal teams provide. However, the ability to articulate these ideas in practical terms can be a difficult feat for a number of reasons.

In today’s modern workforce, analytics play such a vital role in performance management that implementing key performance indicators (KPIs) should not be a question of “if” but rather “when”. But KPIs are not something to rush into or put into place without careful consideration of the ultimate goals of the business, what activities or metrics are the best to monitor, and how the process of data gathering will work.

Done right, implementing KPIs in legal departments can demonstrate value, modify behavior to align with organizational goals and identify needs and trends which can all have a positive, long-term impact on the effectiveness of in-house legal teams. So what exactly are KPIs and how can they be implemented?

What are KPIs?

Key performance indicators, or KPIs measure the performance of a department, company, firm, or business unit. Typically, these metrics use numbers and are tracked over a period of time. KPIs provide targets for teams to aim, milestones to measure progress, and insights that help people across the organization make better decisions.

Writing a clear objective for your KPI is one of the most important parts of developing KPIs. A KPI needs to be intimately connected with a key business objective and an integral part the organization’s success.

Overall KPIs need to be:

Quantifiable and actionable

Measure the factors that are critical to the success of the organization

Directly tied to the business goals and targets

Limited to a small number

Applied consistently

Why are KPIs Important to Measure?

Measuring KPIs enables businesses to understand the performance and health of their team so that critical adjustments can be made to achieve strategic goals. Knowing and measuring the right KPIs will help achieve results faster and more effectively. In-house legal teams create huge amounts of value for an organization, but that story is often lost through ineffective communication. Lawyers think in paragraphs, executives think in metrics. If lawyers can’t convert their ideas and activities into a framework their colleagues can understand, then their story goes untold.

“In-house legal teams create huge amounts of value for an organization, but that story is often lost through ineffective communication. Lawyers think in paragraphs, executives think in metrics. If lawyers can’t convert their ideas and activities into a framework their colleagues can understand, then their story goes untold.”

How are KPI’s Derived?

KPIs should be derived directly from your objectives so that you know how you are performing in accomplishing your goals. Follow the steps outlined below.

The Problems with Measuring Performance

While measuring performance can be excellent for determining the efficiency of legal teams, problems do exist. These can include:

False precision: implausibly precise statistics that create a distorted picture of truth.

Administrative burden: While quality performance measurement and reporting have great potential to improve the quality of a business, these activities can pose a significant administrative burden on participating staff.

Lack of control: Legal has a lack of control over many activities and therefore measuring performance can seem counterproductive to a legal team.

The Solution to Mitigate Problems

KPIs are only really useful when the right ones are identified and implemented in the correct way. To do so, follow these rules:

Less is more. Generally, you should have no more than 3 to ensure a variety of measures without overwhelming the picture. Each business objective should have at least 1 leading indicator and 1 lagging indicator. This allows you to predict future performance as well as record the actual performance and compare these to the direction of your business objective.

Review trends not snapshots. Reviewing trends helps you understand how your business has performed and predict where current business operations and practices will take you. Done well, it will give you ideas about how you might change things to move your business in the right direction.

Benchmark. Every business is different and deals are inherently unique, so you need to create a baseline to measure against. This can be done through benchmarking – taking like things and comparing them to like things in the aggregate rather than only in one specific instanceHere are a couple of ways to establish benchmarks:

Talk to peers and find out what they are measuring and what they are accomplishing

Read reports

Make educated guesses

KPIs don’t need to be perfect. There is no “perfect set” of measures and organizations should experiment with a “starter” set of metrics and evolve these measures over time based on what they learn. What is most important to remember is to regularly review processes with the internal team and management, set defined intervals where you will adjust, scrap or change KPIs as you learn and pair KPIs that measure competing values: e.g., cost & quality, speed & risk.

Sample KPIs

Cost

The reality is that legal budgets are coming under increasing scrutiny and measuring expenditures is easy. However, expenditures are only one part of the cost equation. To provide management teams with a more comprehensive understanding of legal budgets, quantify the value the legal department delivers to the organization. For example, real estate organizations often bill internal legal time to specific assets; make sure to aggregate those billings and present them in the department budget as offsetting the legal expense line items.

Another technique is to offset internal legal expenditures by calculating the costs of outside legal resources that were not used. To do this, each year set a target budget for outside counsel and then measure whether you come in over or under that target. To the extent the legal team is efficient and reduces the amount of outside counsel expenditure, offset those savings against internal legal expenditure.

Quality

Quality is paramount and is often overlooked by management teams because it’s rarely measured. One technique you can use to measure quality is to define a set of positive elements you want to see in your final legal documents and negative elements you don’t want to see in your final legal documents. Give each element positive and negative “points” and then audit your completed deals periodically and compile an aggregate score. Use this too to measure department outcomes, team outcomes or inside versus outside counsel outcomes.

Speed

One of the most important legal department KPIs is the average time to process a deal. This is most commonly captured by measuring a) the time it takes to go from deal approval to when the lease first goes out, and b) from deal approval to signature.

To create more context, supplement speed KPIs with a measure of deal complexity. For example, keep track of how many deals are on the tenant form, size of deals, duration of term, etc. and then over time watch how your speed KPIs vary with your measurement of deal complexity.

Or identify certain blockers that can slow a legal department down and measure those as well. For example, when teams are overworked and processing too many deals the speed metrics may be adversely affected. So in that case plot caseload against speed. Or tenant’s may be a blocker so measure the amount of time deals sit with tenant counsel and plot that against your speed metrics.

Customer Satisfaction

In-house legal teams have a number of stakeholders they serve. These include both internalclients such as the company’s management teams and business units, but also external customers like tenants. To measure internal client satisfaction consider defining a set of attributes business teams value like responsiveness, practicality, accuracy and business sense and then survey the business teams and ask them to score on a scale of 1-5 how they think the legal team performs on each of these criteria.

Assessing external customer satisfaction is tricky because there is tension between the legal team’s obligation to protect their internal client from risk and to make their external customer happy by being easy to work with. It’s impossible, however, to ignore the fact that the external customers keep the lights on, and their satisfaction matters immensely to the ultimate success of any real estate organization. Therefore, measuring how legal teams contribute to overall customer satisfaction is critical. One way to do this is to send out NPS surveys. This simple survey asks a customer to rate on a scale of 1 to 10 how likely they would be to recommend a product or service to a peer.

Another way to measure external customer satisfaction is by surveying tenants and asking them how much they spent on their legal bills. In this context money (and paying less of it) serves as a proxy for customer happiness. For those real estate organizations that use both inside and outside counsel on deals, consider breaking out your tenants’ legal bill for drafting and negotiating leases based on whether the landlord used in-house or outside legal resources. for more on this topic see our post “Making Legal a Profit Center.”

Conclusion

There is no question that legal budgets are under pressure. Lawyers therefore need to communicate the value that they deliver to their companies in terms business leaders can understand. KPIs are a way for lawyers to control the narrative rather than have a narrative imposed on them.

Today, technology is the lifeblood of any business. Technology integration, automation, online ordering and more have become key business strategies, accelerating the shift toward digital transformation. Adopting technologies like these allows businesses to maintain revenue streams while continuing to provide value to customers.

PropTech is no different. Put simply, PropTech is the use of technology to drive efficiencies in real estate, ultimately leading to improved asset returns, reduced friction, and greater transparency. It is rooted in the idea of exploring the digital landscape and adopting new technologies and consumption patterns. Here’s everything you need to know about PropTech.

What is PropTech?

Property technology, or “PropTech,” is the term used to describe the broad application of technology to real estate markets. It refers to the myriad tech companies working to transform the real estate industry, based on a rapidly changing digital landscape and ever-shifting consumption trends and patterns.

PropTech aims to make owning, leasing, or working in a building easier and more efficient for everyone, whether it be through reducing paperwork for property management or streamlining transactions between tenants and landlords.

The PropTech Industry

The rise of PropTech companies around the world is causing a massive shift in the commercial real estate (CRE) industry towards more tech-enabled buildings and work offerings.

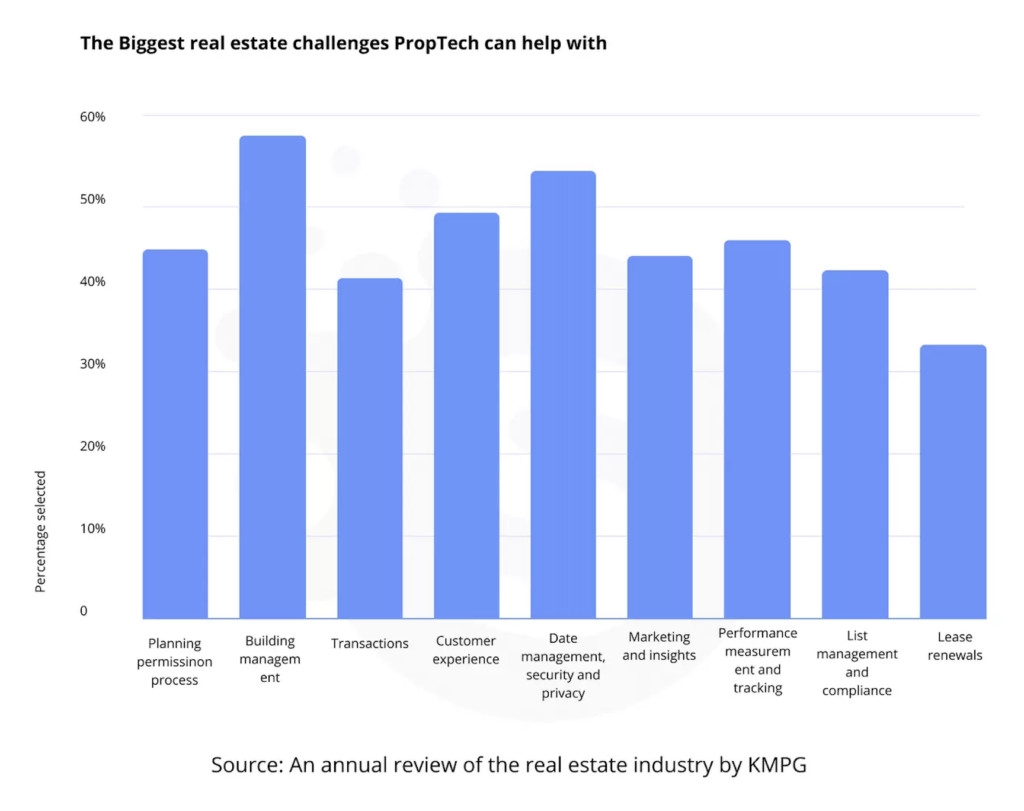

According to the KPMG Global PropTech Survey, the digitally-driven PropTech industry has made considerable progress over the past several years and will continue to do so. Experts have the same technology expectations towards PropTech as other industries like finance, banking, healthcare, and eCommerce.

Why Develop PropTech?

Technological innovation has revolutionized several other industries and now we can’t imagine living without Uber, Venmo, Doordash and so much more. The same benefits — streamlined efficiency, better customer experience, simpler processes — can and should be apparent in the real estate industry. With PropTech, companies are trying to address these pain points and introduce an innovative edge at every step and revitalize existing systems.

How LeasePilot is Changing CRE Tech

LeasePilot is the only company creating a scalable, digital future for commercial real estate leasing. LeasePilot is accelerating the timeframe to close a commercial lease by pairing innovative technology with tried-and-true legal industry standards. Imagine getting a deal done in 10 days that used to take 90. Printing automated abstracts rather than spending countless hours summarizing deal terms. Never re-keying the same information into multiple systems.

Generating transactional reports for lenders, investors, and buyers rather than have lawyers read and re-read the underlying leases ad nauseam.

Ultimately, the impact is radically more efficient markets that free up a massive amount of wasted human potential so it can be re-directed toward pursuing more meaningful objectives.

To learn more about LeasePilot and get the latest on commercial real estate trends

Whether you’re looking to stay on top of the latest CRE news or at the forefront of tech trends, following industry experts on Twitter is one of the best ways to gain up-to-date insight. We’ve compiled a list of the best CRE influencers to follow on LinkedIn and Twitter.

Adam Stanley

Adam Stanley is the Global CIO and Chief Digital Officer at Cushman & Wakefield and is responsible for providing strategic and operational direction for client facing and colleague technology systems across all global business lines. With over 20 years of experience, Adam is a results driven business partner who brings unique expertise to his social platforms.

Founder of theBrokerList.com, Linda is a CRE technology master who covers everything from new technologies and trends to the must-attend conferences in the industry. Linda has created a network of industry professionals including both small and large companies.

Real Estate and CRE tech investor, Jonathan Schultz has combined his passions for real estate and technology as the Co-Founder of Onyx Equities. Jon has used his honest and real approach to become a thought-leader in the CRE tech space.

Chris Ressa is the chief operating officer of DLC Management. Ressa has persistently earned his way to become an established industry influencer and has even been recognized by Chain Store Age by landing on the magazine’s 10 Under 40: Rising Stars of Retail Real Estate list.

Michael Beckerman has had a 25-year career in commercial real estate public relations where he built Beckerman Public Relations into one of the largest firms in the country. Today, Michael serves as CEO of CRETech, the largest event, data and content platform in the commercial real estate tech sector.

Pete Asmus is the CEO and Fund Manager for GREENZONE 360 Asset Management. As a Real Estate Investor, Speaker, Award-winning Radio Host and Author, Pete has built the Largest Commercial Real Estate Group and 2nd largest Real Estate group on LinkedIn

Barbi Reuter is President at Cushman & Wakefield PICOR with over 20 years of senior leadership experience in commercial real estate services. You can find her sharing everything from the latest trend reports to articles on management, business and more.

Lisa Picard is President and Chief Executive Officer of EQ Office, where she leads culture, vision and strategy for the company. She is passionate about curating great spaces that maximize human potential, particularly in this age of rapid automation and technological advancements.